Introduction

Across the industry, preparation for the Anti-Money Laundering Regulation (AMLR) is already underway, but not always in a structured way.

Many organisations are working through interpretations, identifying gaps in their setups, as well as understanding what the regulation means for their AML processes.

At the same time, the day-to-day work for AML professionals remains largely unchanged. This is where AMLR will start to become most visible.

Will risk scoring behave the same way across onboarding and transaction monitoring? Will the data you rely on be consistent across systems? Will decisions be easier to explain, or harder to trace back?

AMLR brings these questions into focus. It connects the parts of the AML process that are often disconnected. And for AML teams, this has a direct impact on the outcome of their work.

In this article, we’ll explore the key changes introduced by AMLR, the new expectations for AML workflows, and the common challenges organisations face as they prepare for implementation.

AMLR: a shared challenge across the industry

AMLR is part of the EU AML Package that affects every regulated entity across the Member States. It introduces a harmonised rulebook, with direct applicability and no national variations.

In theory, the regulation creates an even field for all companies and entities; in practice, it also exposes differences in operational maturity.

Industry discussions and client data show that many organisations have started their journey, but only a small proportion have moved into structured implementation.

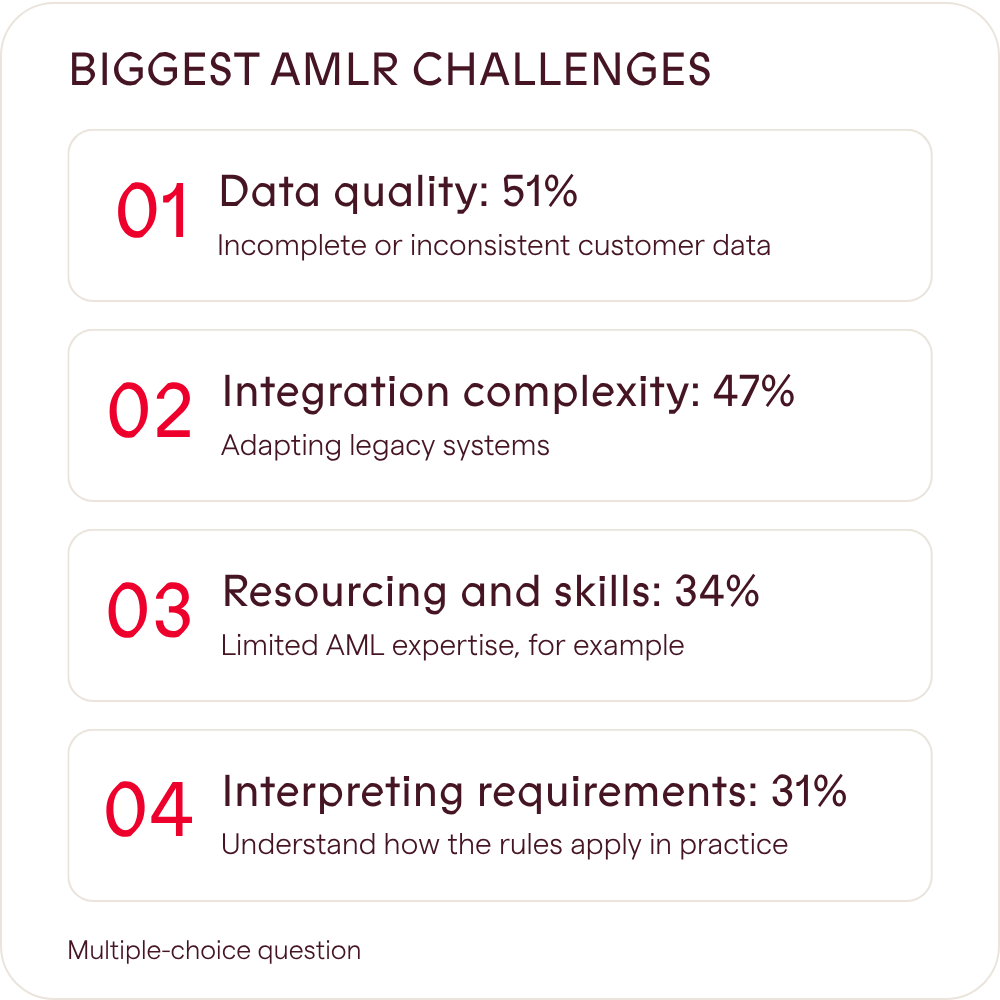

At the same time, many responses point out that AMLR is fundamentally a data problem. 51% see data quality as one of the biggest challenges in preparing for AMLR, followed by:

- Integration complexity (e.g. adapting legacy systems): 47%

- Resourcing and skills (e.g. limited AML expertise): 34%

- Interpreting requirements (e.g. understanding how the rules apply in practice): 31%

- Operational capacity (e.g. alert volumes): 23%

With data forming the basis of the AML lifecycle, AMLR preparation isn’t focused on adjusting individual AML controls, but rather on the entire AML lifecycle: everything from onboarding, CDD, screening, risk scoring, transaction monitoring, all the way to investigations and reporting.

Read more: AMLR readiness 2026 - what it means for compliance teams

Operational changes according to AMLR

Generally, AML teams are familiar with the regulation on a high level, but its operational implications are often underestimated.

AMLR introduces several shifts that directly affect how AML teams must operate:

- A single EU rulebook across jurisdictions: AMLR replaces the fragmented national anti-money laundering rules with directly applicable, harmonised EU requirements for all relevant actors.

- Continuous customer due diligence across the full lifecycle: Companies must dynamically reassess customer and transaction risks throughout the entire relationship, not just at onboarding.

- Faster intervention for high-risk activities, including pre-transaction controls: Especially when it comes to payments, cryptocurrencies, and insurance money, AML checks must be done before funds are moved.

- Stricter requirements on beneficial ownership and PEP identification: Beneficial owners must be verified using multiple sources, while indirect ownership must be aggregated.

- Stronger supervisory powers and clearer accountability at board level: AMLA gains direct supervisory powers, SAR reporting is standardised across the EU, and boards are explicitly accountable for AML effectiveness.

Taken together, these changes reshape AML from a sequence of checkpoints into a continuous, data-driven process.

From fragmented controls to connected workflows

AMLR exposes a structural weakness in many AML setups: fragmentation.

Your current setup might start in a transaction monitoring system, jump into a KYC tool to understand the customer, check screening separately, maybe pull data from yet another source to understand ownership or history. This creates inconsistencies in customer risk scoring, duplication of effort, and limited traceability.

Under AMLR, this fragmentation becomes difficult to justify. Supervisors will focus less on whether controls exist and more on how well they function together. They will assess:

- Whether risk logic is applied consistently across the lifecycle.

- Whether decisions can be explained and reproduced.

- Whether data is reliable and accessible.

- Whether controls are effective in detecting actual risk.

What AMLR readiness looks like

Many might consider preparation for AMLR to be measured by completed analyses, updated policies, and project plans. While these steps remain necessary, they are not sufficient. What will ultimately be assessed is operational performance.

For an AML professional, four capabilities stand out as critical:

1. Consistent risk logic across the lifecycle

Risk models must apply the same definitions, thresholds, and scoring logic across onboarding, ongoing due diligence, transaction monitoring, and investigations.

Disconnected models lead to conflicting decisions - something supervisors will identify quickly.

2. A reliable and unified data foundation

Customer and UBO data must be consolidated, verified, and structured for reuse across all processes.

Data inconsistencies are already a major challenge and are likely to become the single largest compliance risk under AMLR.

3. Continuous, event-driven compliance

Periodic reviews are no longer enough. Risk must be updated dynamically based on transactions, screening hits, and external data changes.

This requires systems that can trigger reassessments and escalate actions automatically.

4. Transparent and traceable controls

Every decision must be explainable: what triggered it, which data was used, and how the outcome was determined.

Under AMLR, audit trails and accessible evidence will be central requirements for an efficient AML lifecycle.

Another important step to take into consideration is to move away from thinking that preparation is an endpoint.

Gap analyses, policy updates, and project plans are starting points. The real work begins when these are translated into operational processes that function consistently in daily use.

Organisations that succeed with AMLR will focus on:

- Testing how their processes work end-to-end.

- Identifying where data or logic breaks down.

- Ensuring that all teams operate within the same workflows.

- Building systems that support continuous compliance, not periodic checks.

The role of technology in AMLR preparation

Meeting these expectations manually is simply not possible. AMLR increases both the volume and speed of required assessments. It also raises the standard for consistency and traceability. This means that your AML system will need to:

- Connect KYC, CDD, screening, and transaction monitoring into one workflow.

- Apply a unified risk model across all processes.

- Update risk in real time as new data becomes available.

- Provide full audit trails for every action and decision.

For example, integrated transaction monitoring can combine customer risk profiles, behavioural data, and configurable rules to detect suspicious activity and prioritise investigations more effectively.

At the same time, structured customer due diligence processes, supported by dynamic questionnaires, automated triggers, and real-time validation, allow you to maintain up-to-date and reliable customer data throughout the lifecycle.

In conclusion - AMLR: a defining moment for AML teams

AMLR represents a significant regulatory shift, but it also creates an opportunity to address long-standing inefficiencies in AML operations.

Many teams already recognise the challenges: manual processes, disconnected systems, and limited visibility across the lifecycle. AMLR brings these issues into sharper focus and raises the expectation that they must be resolved.

The organisations that approach AMLR as an operational transformation, rather than a regulatory exercise, will be better positioned to meet supervisory expectations and improve how their AML programmes function in practice.

Because in the end, AMLR readiness will be measured by how effectively AML works every day, across the entire lifecycle.

Curious how Trapets can help you in your AMLR journey? Our experts are here to help you.